It’s hard to stay committed to your personal, professional, and financial goals when you’re drowning in debt. No matter your income level, overwhelming debt can be paralyzing.

Nonetheless, living in fear is not your only option – there are numerous debt relief strategies that can help you work toward a debt-free life sooner than later. But choosing one can add another layer of confusion and stress: Which one is best for me? What are the risks? What are the benefits and drawbacks?

Help is never more than a phone call away, at least when it comes to understanding your options. Engaging a debt counselor can help you sort through the various debt relief solutions and clear up some of the mystery surrounding them. It’s advisable to seek help sooner than later, especially if you’re having trouble making your monthly payments. Here, though, we will start by breaking down the risks involved with the most common debt relief solutions so that you can assess your options realistically and pragmatically.

Debt Consolidation Loans

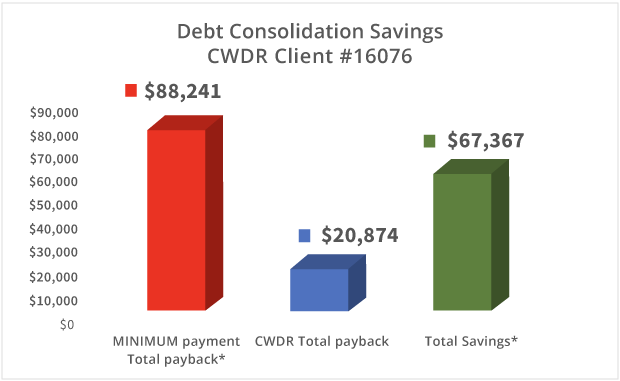

Consolidating your multiple debts into a single amount can be a fantastic way to reduce your stress and simplify your payment schedule, but it’s not without risks.

- Your payoff timeline may be longer, keeping you entrenched in debt and increasing the amount of interest you pay long-term.

- If you don’t close your accounts, you may be tempted to continue to use your credit cards to rack up additional debt.

- If your credit score is weak, you may have trouble utilizing certain types of consolidation solutions, like low-interest personal consolidation loans or home equity loans.

Debt Settlement

Negotiating with your creditors to settle – or forgive – portions of your debt can reduce your overall debt burden, but consider the following consequences:

- The forgiven amount will be considered taxable income, and you will need to report it (and submit a tax payment on it) to the IRS.

- It can negatively impact your credit score.

- It does not resolve the underlying debt issue: Why did you accrue this debt in the first place? Settling debt can tempt some consumers to become complacent and dive straight back into the dangerous spending habits that got them into debt in the first place.

Debt Management

A debt management plan will help you pay your debts in full, often at a reduced interest rate or with certain fees waived. Instead of managing your payments on your own, you will make a single monthly payment to your credit agency, who will pay your creditors on your behalf. However:

- While most debt management plans won’t impact your credit score, closing your open credit accounts will.

- There is little flexibility for missed payments: If you miss one, you will likely be excused from the program or plan.

- Some consumers fall prey to scams. Before you engage a debt management company, do your research and confirm that it’s accredited and reputable.

Bankruptcy

Usually considered a last-resort option, bankruptcy provides a way to wipe out many of your debts if they simply become untenable. In the bankruptcy process, you will work with a federally-appointed trustee to manage your financial decisions and help you navigate the bankruptcy process in a U.S. bankruptcy court.

- Keep in mind that bankruptcy will seriously impact your credit.

- Some debts – like student loans – are not dischargeable in bankruptcy, which means that you will still be on the hook to pay them at the conclusion of your case. It also won’t absolve you from your obligation to pay taxes and child support.

- In Chapter 7, or liquidation, bankruptcy, you will be required to give up all of your property.

- Bankruptcy can severely impact your employment future.

Traps to Avoid

Regardless of which option you ultimately choose, there are a few things you should never do:

- Miss a payment on a secured debt in order to fulfill an unsecured debt – This can result in losing the collateral that secures your initial debt. In other words, don’t fall delinquent on a car payment so that you can make a monthly payment on a hospital bill.

- Withdraw money from your retirement account – Particularly if you’re trying to pay off unsecured debt, this is a bad move. Not only will you face penalties for withdrawing prematurely, but you may deplete your accounts unknowingly in order to stave off increasing debt. You have options to resolve your debt, but no options to replenish your retirement savings (other than continuing to save, trusting the market, and giving it time to build).

- Make decisions based on which creditors are pressuring you the most – Caving under the pressure of creditors can lead you to make poor financial choices, especially if the creditors are acting unethically in their approaches. Contact your accountant, attorney, or credit counselor if you’re stressed about constant contact from a creditor and try to make decisions based on what’s best for you – not based on who’s being the most aggressive.

In short, the best course is always to research your options, to ensure you understand the pros and cons of each, and make the decision that is most suitable for your financial situation, goals, and timeline.